San Diego Home Remodel Insurance: What to Know at Every Stage

Remodeling your home is one of the most exciting improvements you can make. It’s also a major investment. And if there’s one detail I’ve seen San Diego homeowners overlook time and again, it’s insurance.

Whether you’re adding an ADU, reworking your layout, or upgrading finishes, your remodel affects more than just style—it impacts your home’s value and your liability. With wildfire risks, coastal flooding, and San Diego’s strict permitting process in the mix,1 insurance should be part of your planning from the very beginning.

In this guide, I’ll walk you through the key coverage steps at every stage, so you can protect your investment and move forward with confidence.

🎧 Prefer to listen instead? Check out the podcast version of this guide. Perfect for tuning in while you plan your remodel. 👇

🔑 Key Takeaways

- Start With Your Insurer: Contact your insurance provider before any demolition begins. This helps avoid coverage gaps and keeps your home protected throughout the remodel.

- Update Policy Limits: Make sure your coverage accurately reflects the increased value of your home after upgrades or additions.

- Clarify Liability: Find out who holds liability during construction—whether it’s your contractor, their subcontractors, or you.

- Document Everything: Save receipts and take progress photos. These records can support future claims or help with appraisals and resale.

- Consider Specialty Coverage: Depending on the scope of your project, you may need builder’s risk or flood insurance for full protection.

- Peace of Mind Guarantee: Kaminskiy Design and Remodeling offers a two-year warranty on all remodeling projects, giving you added confidence and peace of mind.

- Work With a Local Pro: Choose a local insurance agent familiar with San Diego’s wildfire zones, coastal risks, and permitting requirements.

Insurance Requirements Disclaimer

Important Note: Insurance requirements and coverage options can change frequently based on market conditions, regulatory updates, and carrier policies. While this guide provides general best practices for San Diego homeowners, always verify current requirements and available coverage options directly with your insurance provider or a licensed agent before making any decisions about your remodeling project.

Pre-Remodel Insurance Essentials

Review Your Current Homeowners Policy

Before you start picking out paint colors, call your insurance provider. A remodel can significantly alter the value of your home, and your current policy may not reflect those changes. Policy limits, exclusions, and terms need to be revisited.

Make sure your policy covers:

- Structural changes

- Temporary displacement

- Damage during construction

Understand Policy Exclusions and Gaps

Some homeowners are surprised to find their policies exclude damage during renovations, especially if the property is deemed “vacant” or “unoccupied.” This is especially common in major remodels where you’re living off-site.

What Homeowners Should Know: An unoccupied home under renovation may not be covered for fire, vandalism, or theft. Talk to your insurer about an endorsement or temporary coverage. Ask if your provider offers a “vacancy permit” or rider to bridge the gap.

Get an Updated Appraisal or Valuation

Home improvements, such as adding new square footage or installing luxury finishes, can impact your replacement costs. An updated home appraisal helps your insurance agent set accurate policy limits to match your remodel’s new value. It’s also essential for refinancing and resale down the road.

Consider Increased Personal Property Coverage

If you’re adding new appliances, furniture, or electronics during the remodel, it’s smart to increase your personal property limits. Standard policies may not automatically cover high-value upgrades, such as a smart appliance suite or a built-in home theater system.

Talk with Your Remodeling Contractor

At Kaminskiy, we provide every client with detailed plans and permit records. These can be shared with your insurance agent to ensure proper coverage during the remodel. A design-build firm like ours helps streamline this process.

I always encourage clients to bring their remodel plans to their insurance agent early. It’s one of the easiest ways to prevent costly gaps in coverage.

Contractor Insurance and Documentation

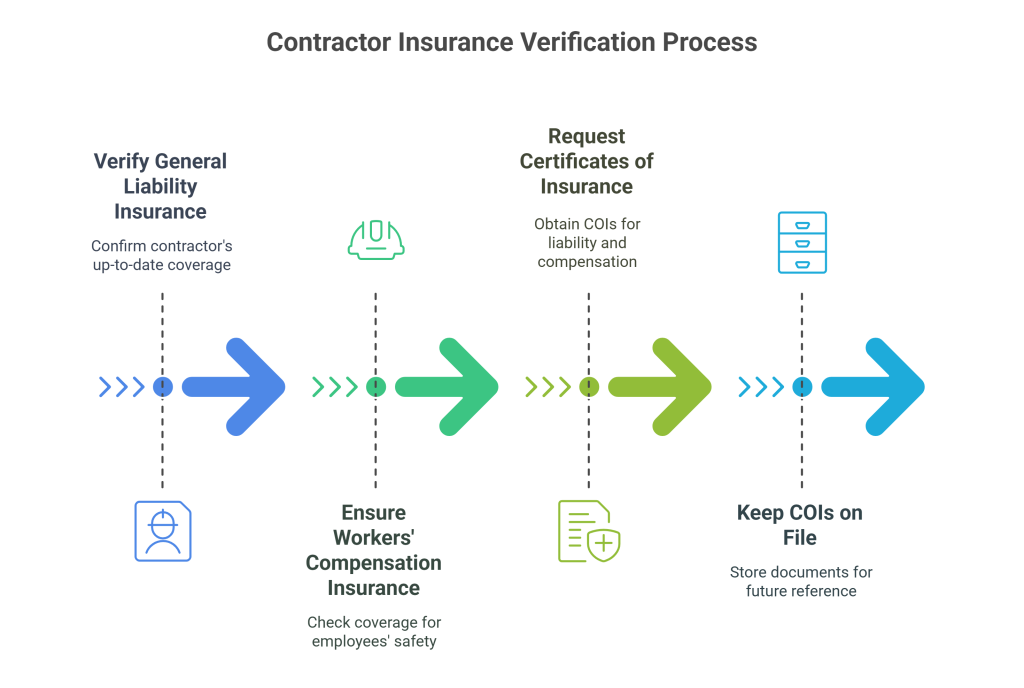

Confirm Contractor’s General Liability Insurance

Verify that your contractor has up-to-date general liability coverage. This protects you if they cause accidental damage to your home or if third-party injuries occur during the project.

Workers’ Compensation Insurance

Ensure your contractor carries workers’ compensation insurance for their employees. Without it, you could be financially responsible if someone gets injured while working in your home.

Request Proof of Insurance

Ask for Certificates of Insurance (COI) and keep them on file. This includes:

- General liability

- Workers’ compensation

- Builder’s risk (if applicable)

Insurance You’ll Need During Construction

Builder’s Risk Insurance: Protection and Scope

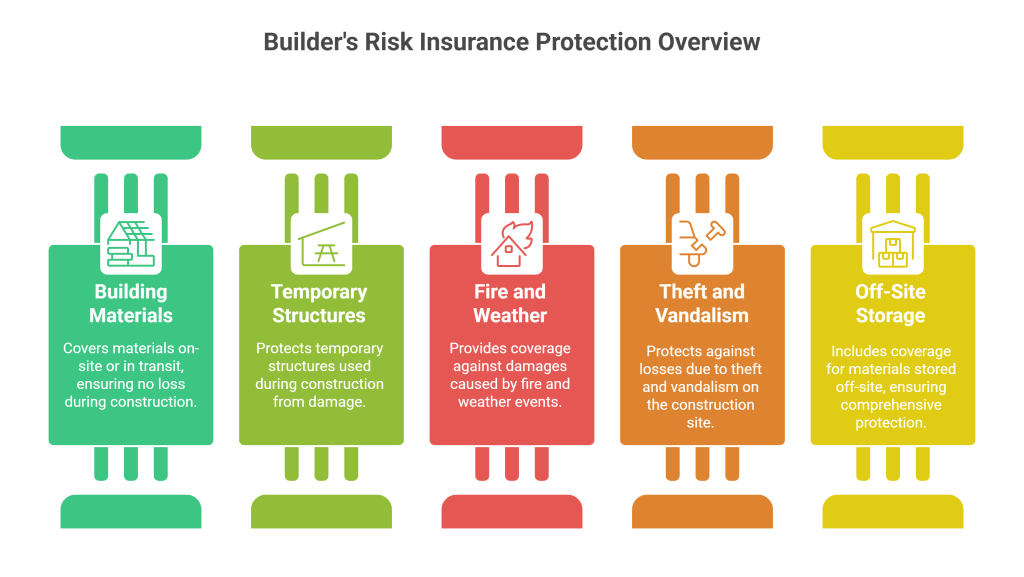

Also known as Course of Construction Insurance, this coverage protects the structure and materials during the remodeling process. It protects against theft, vandalism, fire, and weather-related events.

What It Covers:

- Building materials onsite or in transit

- Temporary structures

- Damage due to fire, wind, theft, or vandalism

- Some policies also include materials stored off-site and on-site equipment

What Builder’s Risk Insurance Typically Doesn’t Cover

Understanding exclusions is just as important as understanding coverage:

- Acts of terrorism

- Normal wear and tear

- Employee theft

- Faulty workmanship, materials, or design

- Earthquakes or floods (unless added)

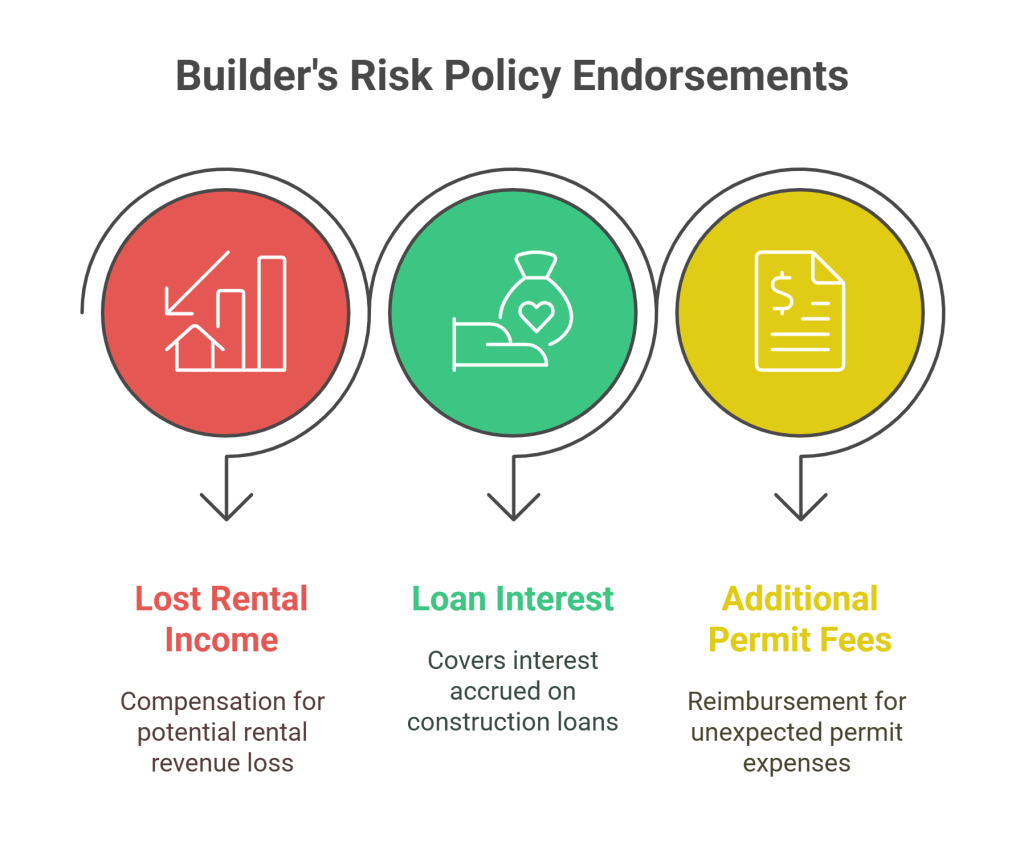

Can It Cover Delays and Soft Costs?

Some builder’s risk policies offer optional endorsements for “soft costs” and delay coverage. These may include:

- Lost rental income

- Interest on construction loans

- Additional permit fees

Speak with your agent about including these if you’re concerned about unexpected delays.

How to Choose the Right Builder’s Risk Policy

Not all policies are created equal. Here’s how to choose the right one:

- Assess the scope of your renovation

- Review coverage limits against your project budget

- Compare deductibles and premium rates

- Look for endorsements relevant to San Diego risks (e.g., wildfire, flood)

- Work with a local agent familiar with regional regulations and weather conditions

📋 Summary Table: Key Considerations for Builder’s Risk Insurance

Before purchasing a policy, here are the essential factors to review with your insurance provider:

Kaminskiy’s Partnership with Buildertrend Saves You More

At Kaminskiy Design and Remodeling, we make every step of your remodel easier, including the insurance process. Through our partnership with Buildertrend Insurance Services, our clients can access Builder’s Risk Insurance with average savings of 20% on equal or better coverage.2

Why choose Buildertrend Insurance through Kaminskiy?

🔹 Unlock better quotes in seven clicks or less

🔹 Personalized one-on-one insurance support

🔹 Access instant policy documents and binders

🔹 Manage coverage and paperwork all in one platform

Liability Insurance and Umbrella Coverage

Even if your contractor is insured, you should maintain robust liability coverage. If a worker gets hurt on your property and the contractor’s policy doesn’t cover it, your insurance may be on the hook.

Permit Compliance and Inspections

Cutting corners on permits can invalidate insurance claims. In San Diego, city inspectors confirm whether your project meets building codes. Noncompliance can void your coverage.

Theft and Vandalism Protections

Remodels are particularly vulnerable to theft, especially when left unattended overnight. Discuss coverage options with your agent for stolen appliances, materials, or tools. Installing cameras or temporary fencing may also lower premiums.

Security Tips:

- Use motion-sensor lighting

- Install temporary fencing or locked storage

- Ask your remodeler about surveillance during off-hours

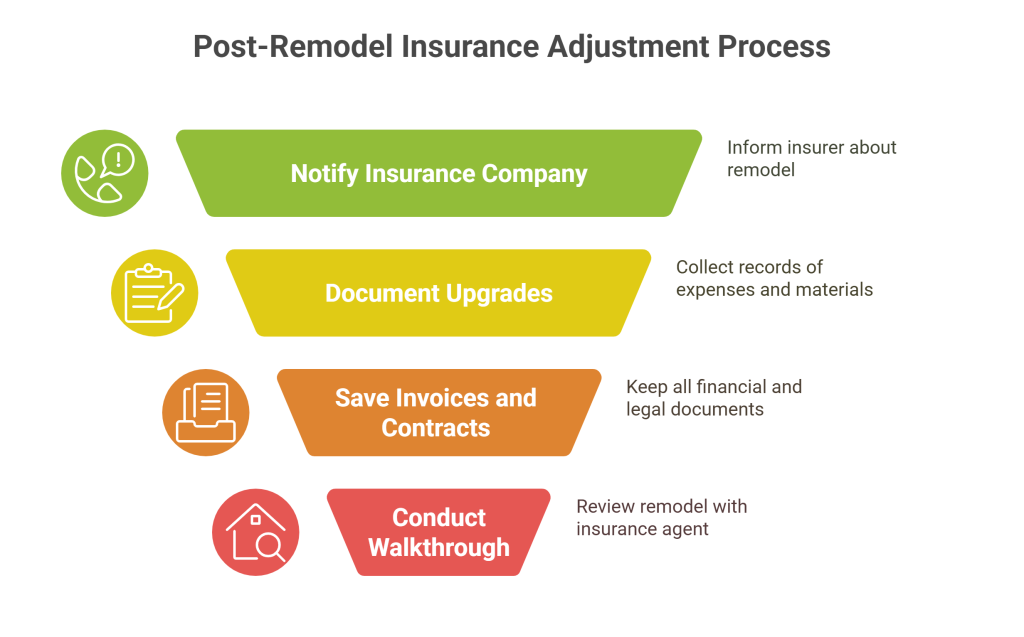

Notify Your Insurance Company

Communicate Changes Early

Let your insurer know about your renovation plans before you begin work. Your project could influence risk factors or premiums. Provide scope, budget, and timeline.

Avoid Claim Denials

Failing to inform your provider can jeopardize coverage if a claim arises during the project. Transparency up front saves major stress later.

Post-Remodel Insurance Adjustments

Update Your Homeowner’s Policy

Once the project wraps up, notify your insurance company. This isn’t just about boosting your coverage—it may even qualify you for discounts, especially if your remodel includes upgraded electrical, plumbing, or fire-resistant features.

Document Every Upgrade

Keep detailed records of expenses, materials used, and before-and-after photos. If you need to file a claim later, this documentation will serve as your best defense.

Do’s and Don’ts:

- Do: Save every invoice and contract

- Don’t: Assume your contractor’s documentation will be enough

Perform a Post-Project Walkthrough with Insurer

Invite your insurance agent for a walkthrough of the finished remodel. This helps ensure coverage is correctly updated and can uncover hidden vulnerabilities or new insurable features.

San Diego-Specific Requirements

Permits and Inspections

Most remodeling work in San Diego requires city permits. The City of San Diego’s Development Services Department outlines the projects that require approval. At Kaminskiy, we handle this process entirely, ensuring your remodel is fully compliant with all relevant regulations.

Verify Contractor Licensing

Only work with licensed contractors registered with the California Contractors State License Board. Licensing is a legal requirement and a safeguard that your contractor meets state-mandated standards.

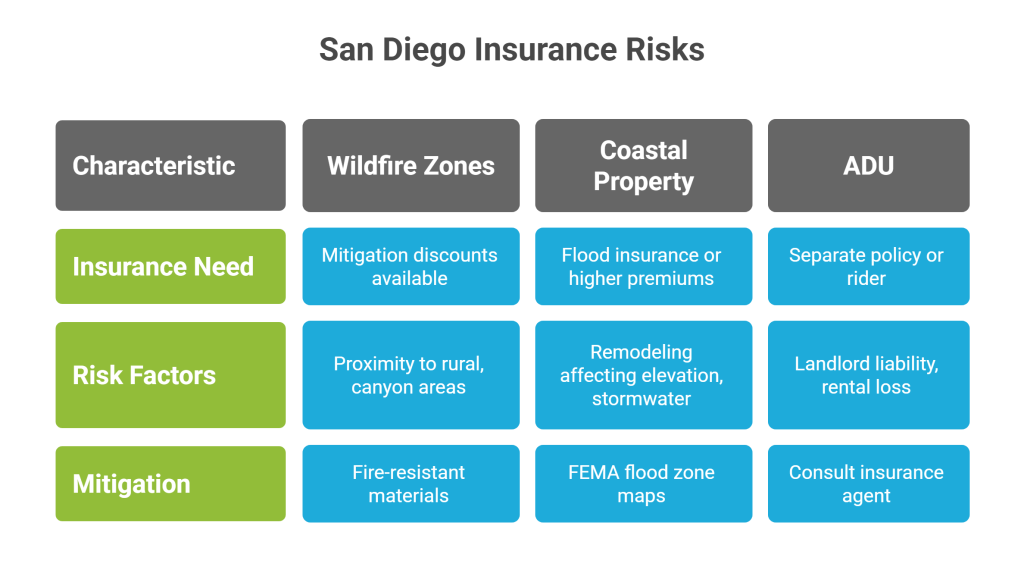

San Diego-Specific Risks to Insure Against

Wildfire Zones

If you added a backyard ADU or expanded your home near fire-prone areas, you may qualify for mitigation discounts, especially if you used fire-resistant materials like fiber-cement siding or Class A roofing.

According to a CalMatters analysis, nearly 3.7 million homes statewide in California are at high or extreme risk for wildfire.3 In San Diego County specifically, many neighborhoods in the backcountry, foothills, and canyon areas face elevated wildfire risk. Take this seriously if you’re near rural or canyon areas, or in communities like Scripps Ranch, Rancho Bernardo, or Ramona.

Coastal Property Flooding

Additions near the coast? You might need flood insurance or higher premiums depending on how the remodel affects elevation and stormwater flow.

Use FEMA’s flood zone maps to check your risk level. Remodeling may change your Base Flood Elevation (BFE).

Building an ADU

ADUs often require a separate policy or a rider. This is especially important if you plan to rent it out. Talk to your agent about landlord liability, rental loss protection, and tenant-related risks.

Working with Insurance Agents

Your best ally during this process is a knowledgeable, local insurance agent. San Diego’s risks—wildfires, earthquakes, coastal flooding—require someone who knows how to navigate local codes and insurance carriers.

Questions to Ask Your Agent:

- Are remodels covered under my current policy?

- Do I need builder’s risk insurance?

- What if I move out temporarily?

- Will my premiums change?

- What endorsements or riders do I need to obtain?

Peace of Mind After the Remodel

At Kaminskiy Design and Remodeling, we don’t just finish the job—we stand behind it. Our full-service design-build process includes a two-year warranty on all our work. If you ever need help providing documentation to your insurer after the project, we’re just a phone call away.

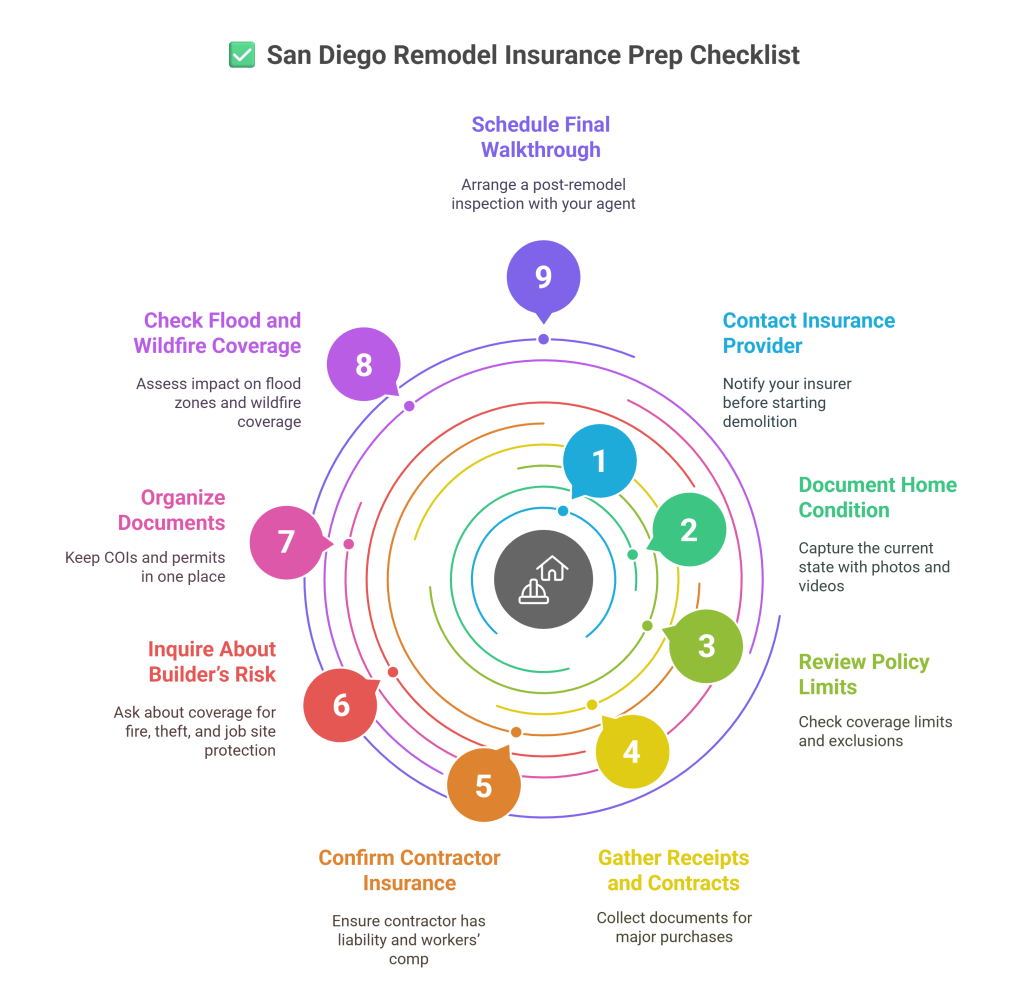

I’ve guided many San Diego homeowners through this process, and I know how overwhelming it can feel. That’s why we created this quick-reference checklist to help you stay organized, protected, and confident from start to finish.

9 Must-Do Insurance Steps Before and After Your San Diego Remodel

Use this quick-reference checklist to ensure your home remodel is fully covered from the start, regardless of the project’s size or scope.

Need help putting this into action? Kaminskiy Design and Remodeling is here to guide you every step of the way, from organizing paperwork to coordinating walkthroughs and documenting your upgrades.

Frequently Asked Questions

How do I choose the right builder’s risk insurance for my remodel?

Start by assessing your renovation’s full scope and value, including materials, labor, and soft costs like permits or rental income loss. Confirm your policy covers common risks in San Diego, such as wildfire, theft, and coastal weather. Ensure your contractor’s insurance doesn’t leave gaps, and work with a local agent who understands regional construction risks.

What insurance add-ons should I consider for a full-coverage remodel?

Depending on your project, consider endorsements for debris removal, equipment breakdown, materials stored off-site, or loss of use. If your home is near a floodplain or wildfire zone, adding flood or wildfire coverage can be essential. These optional add-ons help reduce out-of-pocket costs and claim denials later.

Do I need to adjust my insurance if I’m adding an accessory dwelling unit (ADU) or a rental unit?

Yes. An ADU, especially one intended for rental use, may require a separate policy or rider. Discuss landlord liability, rental income protection, and tenant-related coverage with your agent. Even if you’re not renting immediately, securing appropriate coverage now can save you hassle later.

How does my remodel impact the rebuild value of my home?

Remodels increase your home’s replacement value. Upgrades like new square footage, premium finishes, or smart systems increase the cost to rebuild, which must be reflected in your policy limits. Request an updated appraisal after the remodel to ensure your coverage meets your home’s new value.

What risks should San Diego homeowners insure against during a remodel?

Aside from general construction risks, homeowners in San Diego should factor in wildfire exposure (especially in canyons or foothills), coastal flood risk, and compliance with local permitting regulations. These region-specific risks often require tailored policies or add-ons not included in standard coverage.

What’s the most common insurance mistake homeowners make during a remodel?

Not notifying their insurer before starting work. Failing to update your insurance provider can lead to denied claims or canceled coverage. Always inform them of your project scope and timeline, and request written confirmation of continued coverage.

Remodel with Confidence—We’ve Got You Covered

Insurance isn’t the most exciting part of a home remodel, but it’s one of the most important. With the right coverage in place, you can move forward knowing your investment, your family, and your peace of mind are protected.

At Kaminskiy Design and Remodeling, we take that seriously. We’ll handle permits, help you document your upgrades, and back our work with a two-year warranty. You can count on us to be there every step of the way.

Ready to remodel with confidence?

If you’re ready to get started, I’d love for you to give us a call or schedule your free in-home design consultation. Let’s build something beautiful and make sure it’s protected, too.

Schedule Your Free In-Home Consultation

Additional Resources:

- Permits, Approvals & Inspections | City of San Diego Official Website ↩︎

- Builder’s Risk Insurance Explained – Buildertrend ↩︎

- New California fire hazard maps: What homeowners need to know – CalMatters ↩︎

Kimberly Villa is the Operations Manager at Kaminskiy Design and Remodeling, where she has spent more than a decade involved in projects from pre-design through post-construction. Her experience in the remodeling industry spans nearly two decades across both East Coast and Southern California markets, giving her a firsthand view of how San Diego remodels unfold, from the first budget conversation to the final walkthrough. That day-to-day experience shapes the articles she writes for the Kaminskiy blog, where she helps homeowners make informed decisions before, during, and after a remodel. Before publication, each article is reviewed for accuracy by a Kaminskiy team member with relevant project expertise, such as a licensed architect, certified designer, or project manager.