California ADU Grant and Loan Programs: Your Essential Guide

Last updated on January 2, 2024

California has recently enhanced the ADU Grant and Loan Programs to address the state’s critical need for affordable housing. It’s important to note that as of the latest update, the funds for Phase 2 have been fully allocated, but understanding the program remains crucial for future opportunities.

Accessory Dwelling Units (ADUs), commonly known as granny flats or in-law units, are an innovative solution in this effort. These programs are designed to assist homeowners, particularly those in low-income brackets (with income less than 80% of the Area Median Income), in financing the construction of ADUs on their properties, thus alleviating the housing crisis and providing additional income opportunities.

The California ADU Grant program, managed by CalHFA, offers up to $40,000 (Phase 2) towards predevelopment and non-recurring closing costs for ADU construction. Eligible expenses under this grant include site preparation, architectural designs, permits, soil tests, impact fees, property surveys, and energy reports. In line with recent legislative updates, CalHFA has implemented specific income limits and credit score requirements to ensure that assistance is directed toward needy households. Applicants must own and occupy the property as their primary residence, and the ADU must comply with Fannie Mae/FHA ADU feature requirements and meet all local zoning ordinances.

As part of its ongoing commitment, the state had allocated an additional $25 million (as per Resolution No. 23-13) towards financing ADUs in what is referred to as “Phase 2” of the program. While this funding has now been fully allocated, understanding the structure and benefits of Phase 2 can help prepare for any future phases or opportunities.

This one-time appropriation is part of a strategic move to bolster the program’s reach and effectiveness, particularly in socially disadvantaged areas. The Phase 2 program, which launched on December 11, 2023, has seen significant interest, and its funds have been fully allocated. Prospective applicants should stay informed about the latest developments in the ADU Grant and Loan Programs to be ready for future opportunities.

The CalHFA-approved ADU Participants, including lenders, non-profits, and local government agencies, have had access to reserve funds for the program since its start on December 11, 2023. For comprehensive details about the program’s objectives, the application process, and the upcoming funding phase, interested homeowners are encouraged to visit the official CalHFA website. Interested homeowners must stay informed about the latest developments in the ADU Grant and Loan Programs.

Phase 2 offers renewed opportunities for Californians to contribute to affordable housing solutions in their communities, with a focus on low-income homeowners and a requirement for a Certificate of Occupancy upon ADU completion. While the recent recipients should be aware of potential tax implications, future applicants should also consider this as part of their planning. Receiving benefits from programs like these can result in an IRS income tax form 1099-G. For more detailed information, please refer to the CalHFA Program Bulletin #2023-12.

Key Takeaways

- Focus on Affordable Housing: California’s ADU Grant and Loan Programs are strategically designed to address the affordable housing crisis, and while recent funds have been fully allocated, the strategic focus remains on expanding affordable housing options through future opportunities. These programs enable homeowners, particularly low-income homeowners (with income less than 80% of the Area Median Income), to finance the construction of Accessory Dwelling Units (ADUs), thereby expanding affordable housing options.

- Financial Assistance for Construction: The ADU Grant program has provided substantial financial support, offering up to $40,000 towards costs associated with ADU construction. While the recent funds are fully allocated, understanding the scope of this assistance is crucial for future applicants. This assistance covers a range of expenses, from site preparation to energy reports. Applicants must own and occupy the property as their primary residence, and the ADU must comply with Fannie Mae/FHA ADU feature requirements and meet all local zoning ordinances.

- Targeted Assistance: Managed by CalHFA, the grant program has set income limits and credit score requirements to ensure that financial aid is directed toward homeowners who most need assistance. Prospective applicants should stay informed about any changes to these criteria in future funding rounds. This ensures that the financial aid is directed toward those homeowners who most need assistance. Homeowners interested in creating ADUs can seek the expertise of ADU Design and Builder Contractors to tailor spaces that meet their specific needs while optimally utilizing these grants and loans.

- Updates on the Program’s Future: As of the latest update, all funds for the ADU Grant program’s recent phase were fully allocated. However, the state’s ongoing commitment, evidenced by the additional $25 million allocated for the ADU Loan Program, indicates potential future opportunities. Staying informed about these developments is crucial.

- Phase 2 Rollout: Phase 2 of the program, which began on Monday, December 11, 2023, has seen significant interest, and its funds have been fully allocated. Future phases may continue to focus on alleviating housing hardships and enhancing homeowner equity. Interested homeowners should prepare for these opportunities and be aware of potential tax implications, as they will receive an IRS income tax form 1099-G reflecting the receipt of benefits from the program.

California ADU Grant and Loan Programs 2023 – 2024

In 2023 and moving into 2024, the California ADU Grant and Loan Programs have continued their mission to assist homeowners, particularly those in low-income brackets (with income less than 80% of the Area Median Income), in creating more affordable housing options. While the recent Phase 2 funds have been fully allocated, the programs’ objectives and the need for affordable housing remain as critical as ever.

The California Housing Finance Agency (CalHFA) administers the ADU Grant Program, which has offered up to $40,000 in financial aid for predevelopment costs related to ADU construction. As of the latest update, the funds for the recent phase have been fully allocated, but understanding the scope of this assistance is crucial for future applicants.

In addition to the grant, homeowners can explore various loan programs for financing ADU and JADU projects, including assistance with non-recurring closing costs. These options may continue to evolve, helping to lower the barriers to constructing ADUs and enhancing the capability of homeowners to establish additional housing units.

These include assistance with non-recurring closing costs and helping to lower the barriers to constructing ADUs. These programs collectively enhance the capability of homeowners to establish additional housing units, like ADU conversions, which in turn augment housing availability and present affordable living options for renters.

Marking a significant progression, 2023 saw the introduction of Phase 2 in the ADU Grant Program, backed by an additional $25 million allocation. While this phase’s funds have been fully allocated, it reflects California’s ongoing dedication to expanding the state’s housing supply and addressing the needs of low-income households.

The quick allocation of Phase 2 funds reflects the high demand and California’s ongoing dedication to expanding the state’s housing supply. Future applicants should prepare for these opportunities and be aware of potential tax implications, as they may receive an IRS income tax form 1099-G reflecting the receipt of benefits from the program.

What is a California ADU Grant?

A California Accessory Dwelling Unit (ADU) Grant is a financial assistance program designed to help low-income homeowners (with income less than 80% of the Area Median Income) create more housing units in the state. Eligible homeowners can receive up to $40,000 towards predevelopment and non-recurring closing costs associated with ADU construction1. These costs include site preparation, architectural designs, permits, soil tests, impact fees, property surveys, and energy reports2.

As of the latest update, the funds for the most recent phase have been fully allocated, but understanding the program remains crucial for future opportunities.

ADUs are smaller, independent living spaces on the same property as a primary residence, often equipped with their own kitchen, bathroom, and sleeping area. They are an innovative way to add much-needed housing to California’s limited supply3 and are commonly referred to as granny flats, in-law units, or backyard cottages.

The ADU Grant Program’s main objective is to increase California’s housing supply by covering initial expenses for ADU development. Notably, this grant acts as a reimbursement towards the entire project’s renovation loan and does not require repayment. Recipients should be aware of potential tax implications, as they will receive an IRS income tax form 1099-G reflecting the receipt of benefits from the program.

Differences Between the California ADU Grants Program Phases 1 and 2

ADU Grant Program – Phase 1

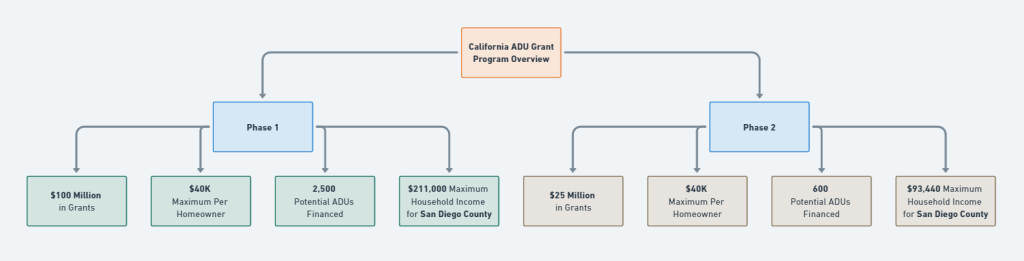

Recap of Phase 1: In 2021, CalHFA was awarded $81 million from the state general fund, with an additional $19 million from its own funds, totaling $100 million for the ADU Program. The program provided $40,000 in grants to low- to moderate-income homeowners for ADU construction.

Source: CalHFA Board of Directors Meeting – 10/26/2023 (California ADU Grant Program – Phase 1 Recap)

Phase 1 Overview:

- $100 Million in Grants

- $40K Maximum Per Homeowner

- 2.5K Potential ADUs Financed

Geographical Information of Phase 1:

- 42% of grants in socially disadvantaged areas

- 42% in Los Angeles County

- Grants issued in 44 of 58 counties

ADU Grant Performance by Region (Phase 1):

- Los Angeles: 63% Permits, 42% Grants

- Bay Area: 15% Permits, 19% Grants

- San Diego: 7% Permits, 10% Grants

ADU Grant Program – Phase 2:

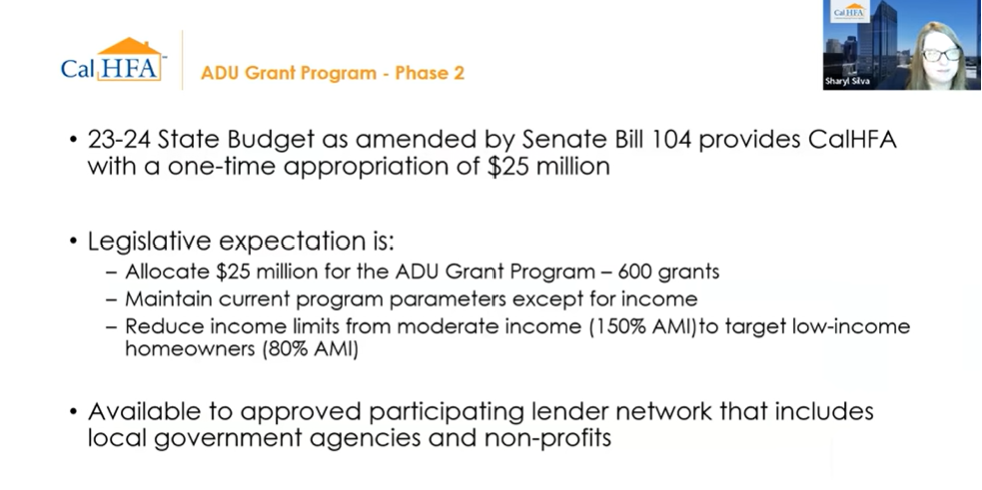

The 23-24 State Budget, amended by Senate Bill 104, provides CalHFA with a one-time appropriation of $25 million for the ADU Grant Program – Phase 24.

While Phase 2 was launched on Monday, December 11, 2023, with a one-time appropriation of $25 million, as of the latest update, these funds have been fully allocated. Interested homeowners should stay informed about any future phases or opportunities.

Source: CalHFA Board of Directors Meeting – 10/26/2023 (California ADU Grant Program – Phase 2)

Phase 2 Overview:

While the potential to finance 600 ADUs under this phase was a significant step, the full allocation of these funds on December 28, 2023, underscores the high demand for such programs. Future applicants should prepare for and stay informed about any new opportunities.

- $25 Million in Grants

- $40K Maximum Per Homeowner

- 600 Potential ADUs Financed

- Targeting low-income homeowners (80% AMI)

- Phase 2 launched on Monday, December 11, 2023

- Funds were fully allocated on December 28, 2023

Participating Lender Network:

While the current phase’s funds are fully allocated, maintaining a relationship with approved lenders and staying informed about their offerings can be beneficial for future opportunities.

- 23 Approved Lenders

- 3 Approved Credit Unions

- 5 Non-Profits

- 4 Local Government Agencies

- Special financing participants in San Diego

For a detailed list of participating lenders and financing partner options, please visit the CalHFA ADU Grant Program Participating Lenders and Special Financing Participants supporting document (Last updated on December 28, 2023).

How do you qualify for the ADU grant in California?

Qualifying for an ADU grant in California requires homeowners to meet certain criteria set by various grant and loan programs, with the CalHFA ADU Grant Program being a primary source of assistance.

Homeowner Requirements

To be eligible for the CalHFA ADU Grant Program, homeowners must adhere to specific income requirements, which vary by county. For Phase 2 of the program, the income limit has been adjusted to target low-income homeowners, specifically those with incomes at or below 80% of the Area Median Income (AMI). For San Diego, the income limit is $93,440.

Additionally, the property must be owner-occupied to be eligible for this financial aid. Homeowners are required to complete and sign the CalHFA Participant Affidavit (Rev 11/27/23) and the CalHFA Applicant Affidavit (Rev 11/27/23).

While the recent Phase 2 funds have been fully allocated, understanding these requirements is crucial for homeowners interested in applying for any future allocations or similar programs.

Property Requirements

- Type of Property: The property must be either a single-family home or a 2-4-unit property.

- Owner-Occupancy: The property should be owner-occupied.

- Income Limits: The ADU grant is only available to low-income homeowners (<80% AMI).

- Compliance with Standards: The ADU must follow Fannie Mae/FHA ADU feature requirements and meet all local zoning ordinances for the use of the property.

- Certificate of Occupancy: A Certificate of Occupancy must be provided upon completion of the ADU, confirming that the unit meets all necessary building and safety standards.

Phase 2 Focus

The recent introduction of Phase 2, backed by a $25 million allocation (as per Resolution No. 23-13), emphasizes support for low-income households. This phase aims to provide broader access to funding for ADU construction in socially disadvantaged areas, promoting equity and community stability.

While the funds for Phase 2 have been fully allocated as of the latest update, the focus on supporting low-income households in socially disadvantaged areas highlights the program’s ongoing commitment to these communities. Interested homeowners should stay informed about any future phases or opportunities.

Additional Programs

Besides the CalHFA ADU Grant Program, there are other initiatives such as the CalHome Program, San Diego Housing Commission ADU Finance Program, Local Early Action Planning (LEAP) Grants, Local Housing Trust Fund (LHTF) Program, Regional Early Action Planning (REAP) Grants, SB 2 Planning Grants, and Community Development Block Grant Program (CDBG).

Homeowners should research these programs’ requirements as well to determine their eligibility. As program details and availability may change, homeowners are encouraged to regularly check the latest information on these and other related initiatives.

In conclusion, obtaining an ADU grant in California involves meeting specific homeowner and property criteria, strongly focusing on supporting low-income families, particularly under the newly launched Phase 2. Homeowners are encouraged to explore the various available programs to find the best fit for their needs and contribute to creating additional housing units on their property.

How do I apply for the ADU Grant?

Where to Apply

To apply for the California ADU Grant Program, prospective applicants should visit the official CalHFA website. The site provides detailed information about eligibility criteria and the application process. The grant offers up to $40,000 towards predevelopment and non-recurring closing costs for constructing an ADU.

As of the latest update, the funds for the most recent phase have been fully allocated. Prospective applicants should continue to visit the official CalHFA website for updates on future funding opportunities and application windows.

Documents Required

Applicants must submit a comprehensive package of documents when applying for the ADU Grant. This includes:

- Proof of ownership.

- Architectural designs.

- Permits and soil tests.

- Impact fees and property surveys.

- Energy reports related to the construction.

- A copy of the current construction loan deed of trust (if financing is used).

- Loan approval documents and escrow instructions.

- An itemized list of pre-development costs.

- CalHFA Participant and Applicant Affidavits.

While the recent funds are fully allocated, gathering and preparing these documents in advance will ensure you’re ready to apply promptly when new opportunities arise. Consulting with ADU professionals can provide guidance through the design, permitting, and construction phases.

Application Timeline

The timeline for the ADU Grant application can vary based on the number of applications received, specific county regulations, and the extent of predevelopment activities your project requires. It’s advisable to start the application process early to allow sufficient time to obtain necessary building permits and complete other pre-construction tasks like site preparation and architectural planning.

While waiting for new funding opportunities, starting early with preparation and understanding your local regulations will position you well for future application windows.

Phase 2 Update

Phase 2, which began on December 11, 2023, with an additional $25 million allocation, has seen its funds fully allocated. Interested homeowners should regularly check the CalHFA website for updates on future phases or similar programs.

CalHFA’s Process

CalHFA will review submitted packages and can contribute a maximum of $40,000 to the construction escrow for building an ADU. These funds are applicable for eligible pre-development costs and non-recurring closing costs. Costs already paid by the applicant won’t be reimbursed as cash but can be used to reduce the principal of the construction loan for the ADU. CalHFA will also issue a Form 1099-G to the borrower in the year they contribute funds to escrow.

While the process described is based on the most recent phase, future applicants should verify if there are any updates or changes in the process for upcoming opportunities.

Engaging ADU Contractors

Working with experienced ADU contractors is crucial for ensuring your project meets program standards. They offer valuable guidance throughout the project, from design and planning to execution, ensuring compliance with all relevant regulations.

In summary, applying for the California ADU Grant involves a thorough preparation of documents and understanding the updated guidelines, especially for the upcoming Phase 2. Staying informed and seeking professional advice will be key to successfully navigating this opportunity.

Benefits of California ADU Grant

Financial Assistance

The California ADU Grant Program offers significant financial support for homeowners aiming to build an Accessory Dwelling Unit (ADU). Eligible homeowners can receive up to $40,000 in reimbursements for predevelopment and non-recurring closing costs associated with ADU construction. This assistance helps cover expenses such as site preparation, architectural designs, permits, soil tests, impact fees, property surveys, and energy reports, making ADU construction more accessible and affordable for many Californians.

While the funds for the most recent phase have been fully allocated, the financial support provided by the program, when available, can significantly ease the burden of ADU construction costs for many Californians.

Increased Property Value

A well-designed and strategically constructed ADU can significantly increase the value of a property. By adding a separate living space with amenities such as a bedroom, bathroom, and kitchen area, homeowners can potentially attract a higher price when it’s time to sell their property. Having a professionally designed ADU, preferably by a knowledgeable architect, can improve the property’s aesthetics and ensure compliance with local regulations, further enhancing the property’s value.

Affordable Housing Solution

ADUs are a practical solution to California’s housing affordability crisis. They offer an economical alternative to traditional housing developments as they don’t entail the high costs of land acquisition and major infrastructure upgrades. For homeowners, ADUs can serve as a source of rental income, while for communities, they provide much-needed affordable rental options. Participation in the ADU Grant Program is mutually beneficial, aiding homeowners financially while contributing to the broader goal of increasing affordable housing availability.

The ADU Grant Program’s contribution to affordable housing remains vital, and interested homeowners should stay alert for future funding opportunities to be part of this solution.

Phase 2 Emphasis

While the additional $25 million allocation for Phase 2 has been fully utilized, the focus on aiding low-income homeowners continues to highlight the program’s commitment to providing affordable housing options. Homeowners interested in future phases should stay informed and prepared.

Community and Economic Impact

By encouraging the development of ADUs, the California ADU Grant Program plays a pivotal role in addressing housing challenges while also offering homeowners a viable option for property enhancement and income generation. The program’s expansion with Phase 2 underscores the state’s ongoing commitment to tackling its housing crisis innovatively and inclusively.

The program’s impact on community and economic development is ongoing. As the state continues to address its housing crisis, staying informed about future phases of the ADU Grant Program and other similar initiatives will be crucial for homeowners looking to contribute to and benefit from these efforts.

Limitations and Challenges

Zoning Restrictions

Navigating zoning laws remains a significant challenge in implementing the California ADU Grant and Loan Programs. Local authorities often have stringent zoning codes that can restrict the construction of new ADUs or impose specific design limitations. These restrictions can hinder homeowners’ ability to fully utilize these programs to create affordable housing solutions.

Despite the California Department of Housing and Community Development’s initiatives to persuade local governments to ease ADU zoning laws, many municipalities remain reluctant. This hesitancy leads to lengthy, sometimes costly, approval processes for homeowners wishing to build ADUs.

Homeowners are encouraged to seek guidance from local planning departments or professional ADU consultants who can provide up-to-date information on zoning regulations and assist in navigating the approval process.

Construction Costs

The financial burden of constructing an ADU is another challenge. While the grant and loan programs cover certain costs like predevelopment and non-recurring closing expenses, the total cost of construction can be substantial, influenced by factors such as material costs, labor rates, and permitting fees. Under the new Phase 2 of the program, the focus on aiding low-income households (80% AMI) may exclude homeowners above this income threshold but still in need of financial support for ADU construction.

For instance, the maximum household income for San Diego County is $93,440 per year. This income threshold varies by county, which may exclude some homeowners who need financial assistance to create affordable housing solutions through ADUs.

With the recent funds fully allocated, homeowners should also explore other financing options and budget carefully for the total cost of construction, keeping in mind the fluctuating prices of materials and labor.

Adapting to New Program Guidelines

The introduction of Phase 2 brings updated program guidelines with a renewed focus on supporting lower-income households. This shift may change the demographic of applicants eligible for the program. Homeowners interested in the program must stay updated on these evolving requirements to ensure they meet the new eligibility criteria.

As program guidelines continue to evolve, staying informed and prepared will be key for homeowners looking to participate in future phases or similar programs.

Impact of Regulatory Hurdles

Prospective participants need to consider the regulatory and financial challenges when planning their ADU projects. While the ADU Grant and Loan Programs aim to promote affordable housing, the realities of dealing with zoning laws and managing construction costs can be overwhelming. Homeowners should carefully assess these challenges against the potential benefits of building an ADU.

Despite these challenges, the long-term benefits of adding an ADU can outweigh the initial hurdles. Seeking advice from financial advisors and ADU experts can provide valuable insights and help homeowners make informed decisions.

Predevelopment Costs for the ADU Grant: An Overview

The California ADU Grant Program offers significant financial support to homeowners for constructing Accessory Dwelling Units (ADUs), focusing particularly on the crucial predevelopment phase. These costs represent the initial expenses incurred before actual construction begins and are vital for ensuring a successful and compliant ADU project.

While the funds for the most recent phase have been fully allocated, understanding these predevelopment costs is crucial for homeowners interested in applying for any future allocations or similar programs.

Key Predevelopment Expenses:

- Site Preparation: This step involves evaluating and preparing the property for ADU construction. It includes clearing debris, land grading, and removing obstacles. Efficient site preparation is crucial for establishing a stable foundation and addressing potential construction challenges.

- Architectural Designs: A fundamental aspect of predevelopment is that architectural designs must align with local building codes, zoning laws, and aesthetic standards. These designs are typically developed through multiple consultations with architects or designers, resulting in detailed blueprints of the ADU’s structure, functionality, and appearance.

- Permits and Approvals: Obtaining necessary permits ensures legal compliance with building, health, and safety regulations. The permit process can be complex, requiring homeowners to navigate various local government requirements.

- Soil Tests and Impact Fees: Soil testing determines the land’s suitability for construction. Impact fees, levied by local authorities, address the infrastructure demands of new development. Both are crucial for assessing the feasibility and environmental impact of the ADU.

- Property Surveys and Energy Reports: Property surveys establish precise boundaries and ideal construction sites on the property. Energy reports are crucial for designing energy-efficient ADUs, which can lead to long-term utility cost savings.

Enhanced Accessibility and Affordability

While the additional $25 million allocation for Phase 2 has been fully utilized, the focus on aiding low-income homeowners continues to highlight the program’s commitment to providing affordable housing options. Homeowners interested in future phases should stay informed and prepared.

Planning for Success

For homeowners contemplating an ADU project, comprehending these predevelopment costs is essential. Consulting with experienced ADU professionals and staying updated on the latest program guidelines is advisable for successfully navigating the application process. This proactive approach can effectively leverage the grant program to create additional, affordable housing options on their properties.

As program guidelines and funding opportunities continue to evolve, staying informed and prepared will be key for homeowners looking to participate in future phases or similar programs. This proactive approach can effectively leverage future grant programs to create additional, affordable housing options on their properties.

Do I have to pay back the ADU grant program?

Understanding the Repayment Terms of the California ADU Grant Program

The California ADU Grant Program plays a pivotal role in helping homeowners build accessory dwelling units (ADUs) on their properties. A key feature of this program is the nature of the funding: it provides grants, not loans, which significantly eases the financial burden on recipients as these funds do not require repayment.

Grant Details:

- Homeowners can secure up to $40,000 to cover predevelopment and non-recurring closing costs related to ADU construction.

- These grants cover a variety of expenses, such as site preparation, architectural designs, permits, soil tests, impact fees, property surveys, and energy reports1.

- The grant acts as a reimbursement credited towards the overall renovation loan of the ADU project.

Eligibility and Compliance:

- To be eligible, applicants must typically own and occupy the property where the ADU will be constructed.

- The program adheres to the California Health and Safety Code, Section 65583(c)(7), which encourages local governments to support ADU development.

- The updated ADU financing laws, effective from January 1, 2021, have streamlined the ADU construction process, enhancing the utility of the grant.

Recent Legislative Updates:

- With the launch of Phase 2 of the ADU Grant Program, as per Senate Bill 104, there has been a shift in focus to assist low-income households (80% AMI).

- This phase allocates $25 million toward financing 600 ADUs, indicating a strategic approach to make ADUs more accessible to lower-income groups.

While the funds for Phase 2 have been fully allocated, the program’s continued focus on assisting low-income households highlights the importance of staying informed about future phases or similar initiatives.

Impact and Benefits:

The ADU Grant Program, especially with its updated focus and increased funding, represents a significant effort by the state of California to expand affordable housing options2. By removing the requirement for repayment, the program lessens financial barriers for homeowners, encouraging the construction of ADUs. This not only aids in alleviating the housing crisis but also promotes community stability and increases housing diversity.

For homeowners considering building an ADU, understanding the grant’s no-repayable nature can be a key deciding factor. It offers a practical solution to expand living space, generate rental income, or accommodate family members, contributing positively to both individual households and the broader community.

Recognizing that the grant does not require repayment can significantly alleviate financial concerns for homeowners, making the prospect of building an ADU more attainable and appealing.

- ADU Grant Program | CalHFA – California

- Accessory Dwelling Units | California Department of Housing and Community Development

If I already have funds, can I still receive a grant for the ADU program without refinancing/applying for a construction loan?

Yes, homeowners who already have funds for their ADU project can still receive a grant without refinancing or applying for a construction loan. The California Housing Finance Agency (CalHFA) offers a $40,000 grant to help low-income homeowners cover pre-construction costs associated with building an Accessory Dwelling Unit (ADU).

Navigating the ADU Grant Program with Existing Funds

A significant advantage of the California ADU Grant Program is its flexibility, particularly for homeowners who already possess funds for their ADU project. The California Housing Finance Agency (CalHFA) extends a $40,000 grant to facilitate the construction of Accessory Dwelling Units (ADUs), even for those who don’t need additional financing through loans.

While the funds for the most recent phase have been fully allocated, understanding how the grant can complement existing funds is crucial for homeowners interested in applying for any future allocations or similar programs.

Key Aspects of the Grant:

- The grant primarily aims to reimburse predevelopment and non-recurring costs related to ADU construction, such as site preparation, architectural designs, permits, and soil testing.

- Homeowners who have adequate funds for their ADU project can still apply for and benefit from the grant. This approach helps reduce the overall financial impact of ADU construction.

Applying for the Grant:

- The application process for the grant is independent of the need for refinancing or a construction loan.

- Homeowners should approach organizations like the California Community Economic Development Association (CCEDA) for guidance on eligibility and assistance in accessing the grant.

Homeowners should regularly check the official CalHFA website or consult with organizations like CCEDA for the most up-to-date information on eligibility and the application process.

Eligibility and Compliance:

- It’s crucial to understand and adhere to the guidelines of the CalHFA grant program to ensure compliance and eligibility.

- The program’s focus on aiding low-income households, especially in its second phase, requires applicants to meet specific income criteria.

As the program continues to evolve, staying informed about the latest guidelines and funding opportunities will be key for homeowners looking to participate in future phases or similar programs.

Strategic Benefits:

- This grant offers significant support for homeowners who wish to develop ADUs but are deterred by the financial implications.

- By eliminating the need for additional loans or refinancing, the program encourages more homeowners to undertake ADU projects, contributing to the larger goal of increasing affordable housing.

Phase 2 Considerations:

- While the additional $25 million allocation for Phase 2 has been fully utilized, the program’s continued focus on assisting low-income households highlights the importance of staying informed about future phases or similar initiatives.

Is the ADU grant program still available in California?

Current Status of the California ADU Grant Program

The California Accessory Dwelling Unit (ADU) Grant Program has seen significant updates and developments in 2023. Here’s what you need to know about its current availability:

Previous Funding and Program Pause:

- As of March 1, 2023, all initial funding for the ADU Grant Program was fully reserved. This led to a temporary pause in accepting new applications due to the high demand and the need for additional resources to meet the ongoing demand for affordable housing solutions.

- Applicants affected by this pause are encouraged to stay informed about any future funding or program resumptions.

Additional Funding and Phase 2 Launch:

- Although the additional funding for Phase 2 has been fully allocated, California’s commitment to affordable housing solutions remains strong. Homeowners interested in the program should stay alert for announcements regarding future phases or additional funding.

Phase 2 Details and Expectations:

- Launch Timeline: The Accessory Dwelling Unit (ADU) Grant Program Phase 2, which launched on December 11, 2023, is now actively assisting homeowners.

- Target Audience: This phase specifically focuses on low-income homeowners (80% AMI), aiming for a more targeted impact in the affordable housing sector.

- Application Process: Prospective applicants are advised to monitor the official CalHFA website for the most current information on application dates and eligibility criteria. For direct inquiries, contact the CalHFA Single Family Lending Division at (916) 326-8033 or by email at [email protected].

As the landscape of the ADU Grant Program continues to evolve, staying up-to-date with the latest information and preparing your application materials in advance will be crucial for participation in any future phases.

Strategic Focus of Phase 2:

- Phase 2 underscores California’s dedication to alleviating the housing crisis by facilitating ADU development, with a particular focus on aiding socially disadvantaged areas.

Despite reaching its funding capacity in the initial phase, the launch of Phase 2 signifies California’s ongoing efforts to support affordable housing. Homeowners considering ADU development are encouraged to stay informed and prepare for future opportunities to participate in this valuable program.

Besides the ADU grant program, how can I get funds to build an ADU in California?

Exploring Financing Options for ADU Construction in California

California’s commitment to expanding affordable housing options extends beyond the ADU Grant Program. Homeowners looking to build Accessory Dwelling Units (ADUs) have access to a variety of financing sources, accommodating different financial circumstances and project needs.

Diverse Loan Opportunities:

- Home Equity Loans and Lines of Credit: These are popular choices for homeowners with sufficient equity in their primary residence. They allow you to borrow against the value of your home to finance ADU construction.

- Refinance Loans with Cash-Out Option: This option involves refinancing your current mortgage and taking out the difference in cash, which can be used towards ADU development.

- RenoFi Loans: As highlighted in a recent RenoFi article, these loans combine the after-renovation value of your property and your current mortgage, providing a significant loan amount with manageable payments. This can be especially advantageous for extensive ADU projects.

- Personal Loans and Savings: For smaller-scale projects, personal savings or unsecured personal loans might be viable options, although they typically come with higher interest rates.

Before opting for any loan, it’s advisable to consult with a financial advisor to understand the implications fully and choose the option that best suits your financial situation and project needs.

State and Local Programs:

- California Department of Housing and Community Development (HCD) ADU Programs: These initiatives are specifically tailored to support ADU constructions, offering financial assistance and resources to streamline the process.

- Local Government and Non-Profit Programs: Various localities in California offer their own ADU financing programs, often with specific focus areas or populations in mind. These can include low-interest loans, grants, or technical assistance for eligible homeowners.

As program details and availability may change, regularly checking the HCD website and local government resources for the latest information is recommended.

Recent Developments:

- Phase 2 of the CalHFA ADU Grant Program: While the funds for Phase 2 have been fully allocated, the program’s network of approved lenders and the focus on low-income households may inspire similar future initiatives. Keeping an eye on such developments can provide additional opportunities for financing your ADU project.

California homeowners considering ADU construction have multiple financing routes to explore. From leveraging home equity to taking advantage of state and local programs, these options cater to different financial situations and ADU project scales. Staying informed about the latest developments in state funding and loan programs is crucial in making the most out of these opportunities.

What loan programs does CalHFA offer?

CalHFA Loan Programs and Their Relevance to ADU Financing

The California Housing Finance Agency (CalHFA) offers a suite of loan programs aimed at assisting low-to-moderate-income families in achieving homeownership, which can also be relevant for those considering ADU projects.

Core Loan Programs:

- CalPLUS Conventional Loan Program: This program combines an affordable fixed-rate mortgage with a zero-interest program (ZIP) for down payment assistance, making it a viable option for first-time homebuyers. Homeowners considering an ADU could potentially use this program for initial home purchase or refinancing, creating a foundation for future ADU development.

- First-time Homebuyer Assistance Programs: Including the MyHome Assistance Program and the School Teacher and Employee Assistance Program, these provide deferred payment loans for down payments and closing costs. These programs could be instrumental for new homeowners planning to build ADUs on their newly purchased properties.

- Energy Efficient Mortgage (EEM) Program: This encourages energy-efficient home improvements. For ADU builders, this could mean additional funding for sustainable ADU designs, aligning with California’s green building standards.

Homeowners interested in these programs should consult the official CalHFA website for the most up-to-date information on eligibility, terms, and application procedures.

ADU-Specific Considerations:

- Interaction with ADU Financing: While CalHFA’s primary focus is on home purchasing, the structure of these loans might allow for their use in conjunction with ADU development, especially for homeowners who recently purchased their property and are looking to add an ADU.

- Leveraging Loan Programs for ADU Projects: Homeowners could potentially use these loan programs to strengthen their financial position, making them more eligible for ADU grants or other financing options for ADU construction. In addition to leveraging CalHFA loan programs, homeowners should stay informed about any ADU-specific financing options or grants that may complement these loans, providing a more robust financial foundation for their ADU projects.

When considering these loan programs for ADU projects, it’s advisable to consult with a financial advisor or a loan officer who can provide guidance on how to effectively integrate these funds into your ADU development plan.

CalHFA’s loan programs offer valuable opportunities for low-to-moderate-income families in California, not just for home purchasing but also as potential stepping stones for ADU projects. By understanding the interaction between these loan programs and ADU financing, homeowners can better navigate their options and plan effectively for their ADU development.

What is the difference between CalHFA and FHA?

Distinguishing CalHFA and FHA in the Context of ADU Financing

The Federal Housing Administration (FHA) and the California Housing Finance Agency (CalHFA) both play pivotal roles in facilitating affordable housing. Yet, they serve distinct functions that are particularly relevant to those considering ADU projects.

FHA’s Role: FHA, a federal entity, primarily provides mortgage insurance, backing loans made by approved lenders. This support is crucial for first-time homebuyers and low-to-moderate-income borrowers, offering more lenient credit and down payment terms. FHA-insured loans can be used for purchasing homes that might include ADUs or for refinancing purposes that could free up funds for ADU construction.

Homeowners interested in FHA-insured loans should consult with approved FHA lenders to understand the specific terms, benefits, and suitability of their ADU projects.

CalHFA’s Specialized Focus: CalHFA caters specifically to California’s unique housing needs. It offers mortgage assistance and direct grant programs for ADU construction.

While the recent $25 million allocation for CalHFA’s ADU grant program has been fully utilized, the agency’s ongoing commitment to California’s housing needs suggests potential future opportunities. Interested homeowners should stay alert for any announcements regarding additional funding or programs.

Impact on ADU Projects:

- FHA Loans for ADU Projects: While not directly offering ADU-specific programs, FHA loans can be instrumental in the initial purchase of properties suitable for ADU development or in refinancing existing properties to fund ADU construction.

- CalHFA’s Direct Support for ADUs: CalHFA offers more direct support for ADU projects through its grant programs. These grants can significantly lower the financial barriers to ADU construction, specifically targeting Californians looking to add ADUs to their properties. Recipients should be aware of potential tax implications, as a Form 1099-G may be issued for the grant amount.

Prospective ADU builders should consider how FHA loans and CalHFA grants might complement each other, potentially combining resources from both to create a more comprehensive and effective financing strategy for their ADU projects.

Understanding the differences between CalHFA and FHA is crucial for Californians exploring options for ADU projects. While FHA provides a broader, nationwide support system for affordable home purchasing, CalHFA offers more targeted assistance for ADU construction within California. Prospective ADU builders should consider both options to maximize their resources and opportunities for successfully completing their ADU projects.

What are the income limits for the California ADU Loan Program?

Updated Income Limits for the California ADU Grant Program

The income limits for the California ADU Grant Program play a crucial role in determining eligibility for homeowners in San Diego and across the state. These limits vary by location and household size, focusing on supporting low-income families. Here’s what San Diego homeowners need to know:

CalHFA ADU Grant Program: Managed by the California Housing Finance Agency (CalHFA), this program offers up to $40,000 towards predevelopment and non-recurring closing costs for the construction of ADUs. Eligible expenses under this grant include site preparation, architectural designs, permits, soil tests, impact fees, property surveys, and energy reports.

While the recent allocation for the CalHFA ADU Grant Program has been fully utilized, understanding the income limits is crucial for homeowners interested in applying for any future allocations or similar programs.

Income Eligibility Based on AMI: Eligibility for the grant is now targeted towards low-income homeowners, specifically those earning up to 80% of the Area Median Income (AMI) as set by HUD. This recent adjustment is designed to help households most in need of affordable housing solutions.

As AMI figures are subject to annual adjustments, homeowners should verify the most current income limits through official resources like the HUD User website or CalHFA.

San Diego Specifics: In San Diego County, for the year 2023, the maximum income limit for a household of four to qualify as low income (less than 80% AMI) is approximately $93,440. This figure provides a guideline for San Diego residents to assess their eligibility for the grant program.

For the most accurate and current income limits applicable to your county, consult your local housing authority or the CalHFA website.

County-Wide Variations: It’s important to note that income limits differ from county to county. Homeowners should refer to the 2023 Low-Income Limits (<80% AMI) for the CalHFA ADU Grant Program for a clear understanding of their specific county’s limits. For instance, in Los Angeles County, the maximum income limit is $84,160, while in San Francisco, it is $126,560.

Utilizing HUD User Website: For an in-depth view of AMI guidelines across various regions, the HUD User website remains a valuable resource. This site offers detailed information to help applicants determine their qualification status based on their location and household size.

Understanding and adhering to the income limits is a critical step in applying for the California ADU Grant Program. Homeowners interested in constructing ADUs should utilize the provided resources to assess their eligibility and take the first step toward building a cost-effective and valuable addition to their property.

What credit score is necessary to qualify for a CalHFA loan?

Credit Score Requirements for CalHFA Loans and ADU Financing

Understanding the credit score requirements for CalHFA loans is crucial for first-time homebuyers and those considering building an ADU in California, including San Diego. Here are the key points:

- Minimum Credit Score: For government loan programs offered by CalHFA, such as CalHFA FHA and CalPLUS FHA, the minimum credit score required is 640. However, specific scenarios might necessitate a higher score of 660, especially for manually underwritten loans and loans for manufactured housing. It’s important to verify the most current credit score requirements with CalHFA or an approved lender, as these criteria may be subject to change.

- Co-Borrower Requirements: This credit score requirement applies to all parties on the loan, including co-borrowers. Also, all borrowers must occupy the home and meet the definition of a first-time homebuyer for CalHFA Conventional loans. All borrowers should be aware of their credit status and how it affects their eligibility for a CalHFA loan, especially when considering co-borrowing.

- Credit Score Assessment: Lenders typically use the middle score of the lowest-scoring borrower for eligibility purposes. If only two scores are available, the lower one is used.

- Other Eligibility Criteria: Besides the credit score, applicants need to comply with other requirements, such as income limits and citizenship. Notably, if rental income from an ADU is part of the loan qualification, CalHFA will use the gross rental income for compliance assessment. Applicants should review all eligibility criteria, including income limits and citizenship requirements, to ensure they meet the qualifications for a CalHFA loan.

- ADU Financing Connection: For homeowners in California considering an ADU project, understanding these credit requirements is important. A good credit score can facilitate obtaining a loan for a primary residence and may also impact the financing options for an ADU. Specifically, a strong credit score can enhance eligibility for loans and grants related to ADU construction.

- Application Process: To apply, contact a CalHFA-approved lender who can provide guidance based on specific loan program requirements. Before contacting a CalHFA-approved lender, prepare your financial documents and credit information to facilitate a smooth application process.

How much can I get with CalHFA?

ADU Grant Program – Updated Information as of October 2023

The California Housing Finance Agency’s (CalHFA) ADU Grant Program continues to support homeowners by providing up to $40,000 towards predevelopment and non-recurring closing costs in the construction of Accessory Dwelling Units (ADUs). These costs encompass a range of pre-construction necessities, including site preparation, architectural designs, permits, soil tests, impact fees, property surveys, and energy reports. It’s important to note that the grant amount may vary depending on the homeowner’s specific needs and project details.

Homeowners interested in the grant should consult with CalHFA or an approved lender to understand the specific grant amount they may be eligible for based on their project details and needs.

Program Updates (As of October 26, 2023): The CalHFA Board of Directors recently approved the details for the second round of ADU Grant funding. A key update in this phase is the adjustment of applicant income limits to 80% of the Area Median Income, focusing the program on assisting low-income homeowners. The full list of Approved Participants (Last updated on November 20) is available, and the program opened for new reservations on December 11, 2023, following an official announcement in mid-November.

As program details and availability may change, regularly checking the CalHFA website for the most up-to-date information is recommended.

About ADUs: ADUs, commonly known as granny flats, in-law units, backyard cottages, or secondary units, offer a practical and affordable solution to California’s housing shortage. They serve as independent living spaces on the same property as a primary residence, often complete with essential amenities.

For the latest updates on the ADU Grant Program, including lender information and application guidelines, please visit the CalHFA ADU page.

What are the interest rates for the CalHFA loan program?

The California Housing Finance Agency (CalHFA) offers various loan programs to assist homebuyers in achieving their dream of homeownership. One such program is the CalHFA Conventional Program, which provides a fixed interest rate for a 30-year term.

Interest Rate Variability: Interest rates for CalHFA loan programs can vary depending on the specific program and market conditions. For example, the CalPLUS Conventional program includes a 3% Zero Interest Program (ZIP) for eligible homebuyers, offering a deferred payment loan with a 0% interest rate for a portion of their down payment or closing costs. For personalized rate information based on your specific circumstances, it’s advisable to consult with a CalHFA-approved lender who can provide detailed guidance.

CalHFA FHA Loan Program: The CalHFA FHA loan program, an FHA-insured first mortgage, offers a slightly higher 30-year fixed interest rate than the standard FHA program. It is combined with the CalHFA Zero Interest Program (ZIP) for closing costs, providing valuable financial assistance to eligible homebuyers.

Regular Rate Updates: It is important to note that interest rates for CalHFA loan programs may change periodically. Potential borrowers should consult the CalHFA Rates page for the most up-to-date interest rate information.

Factors Influencing Rates: Individual interest rates may also be influenced by factors such as your credit score and debt-to-income ratio. These factors can significantly impact the rate offered, and potential borrowers should consider them when applying for a loan.

Understanding how your credit score, debt-to-income ratio, and other financial factors influence your offered interest rate is crucial. A financial advisor or loan officer can provide insights into optimizing your financial profile for the best possible rate.

Summary: The CalHFA loan program offers various fixed-rate mortgage options to assist homebuyers in California. Interest rates may vary depending on the specific program and individual financial situation. The CalHFA Conventional program, CalPLUS Conventional program, and CalHFA FHA loan program are some examples, each with its own interest rates and financial assistance options.

Can a buyer combine a CalHFA loan with a 203k program?

Yes, a buyer can combine a CalHFA loan with a 203k program. The 203k program is a special FHA loan that allows homebuyers to finance both the purchase of a home and the cost of its rehabilitation through a single mortgage.

CalHFA and 203k Integration: CalHFA recently added the option to use a limited 203k as part of their offerings. This allows buyers to roll the costs of minor remodeling and non-structural repairs into their mortgage payment, with up to $35,000 available for eligible repairs.

To ensure a smooth integration of a CalHFA loan with the limited 203k program, it’s crucial to consult with CalHFA-approved lenders who are experienced in handling both loan types.

Focus of the Limited 203k Program: The limited 203k program focuses on minor renovations that do not involve major structural changes or additions to the property. Examples of eligible improvements include:

- Updating kitchen appliances

- Replacing flooring

- Repairing or replacing a roof

- Improving electrical, plumbing, or HVAC systems

- Painting, both interior and exterior

- Adding or replacing windows and doors

The scope of eligible improvements under the limited 203k program may vary. Consulting with a 203k consultant will provide a comprehensive assessment and ensure that your planned renovations comply with the program’s guidelines.

Working with Loan Officers and 203k Consultants: It is crucial for buyers to work with a knowledgeable loan officer to determine their eligibility for a CalHFA loan and understand the specific requirements of the limited 203k program. Loan officers can also help buyers pre-qualify for a loan amount, providing an estimate of how much they can afford. Additionally, a 203k consultant is essential in assessing the scope of work and ensuring that the renovations comply with the guidelines of the limited 203k program.

Seeking loan officers and 203k consultants with experience in both CalHFA loans and 203k programs can provide you with the best guidance and help streamline the financing process.

Combining Financing Options: By combining a CalHFA loan with a 203k program, buyers can access financing options that cater to their unique needs, making homeownership and necessary home improvements a more attainable goal.

Can I still qualify (meeting all other requirements) if I use a “co-borrower” or “co-signer” for CalHFA FHA Loans?

For individuals looking to finance an Accessory Dwelling Unit (ADU) in California through a CalHFA FHA Loan, understanding the role of co-borrowers and co-signers is crucial. Co-borrowers are equally responsible for the loan and hold ownership of the property, while co-signers guarantee the loan but do not have property ownership.

CalHFA’s Policy on Co-borrowers and Co-signers: According to the latest CalHFA guidelines, the agency has specific restrictions regarding the use of non-occupant co-borrowers and co-signers in their loan programs, including FHA Loans. This policy is designed to maintain the focus of their programs on assisting low- to moderate-income borrowers.

As policies may change, it’s important to review the most current CalHFA guidelines or consult with a CalHFA-approved lender to understand the latest on co-borrower and co-signer eligibility.

Understanding Funding Laws and Regulations: Potential borrowers must be aware of the funding laws and regulations in California, which include income and loan limits, as well as specific eligibility criteria. These regulations ensure that financial assistance is directed toward those most in need.

Understanding how funding laws and regulations apply to your specific situation, especially when considering a co-borrower or co-signer, is crucial for ensuring compliance and eligibility.

Exploring Alternative Financing Options: For those who may not meet these requirements, alternative financing options are available. Exploring other loan programs or complying with CalHFA’s specific eligibility criteria, like meeting the minimum credit score and debt-to-income ratio, can be viable paths to financing ADU projects.

Consider a wide range of financing options, including other state or local programs, to find the best fit for your financial situation and homeownership goals.

Seeking Professional Guidance: If you’re considering financing an ADU project, consulting with a knowledgeable mortgage professional is highly recommended. They can provide valuable insight into various financing options and help identify the best approach for your situation, ensuring compliance with funding laws and aiding in achieving your homeownership and property development goals.

Is it possible to refinance a CalHFA loan?

Yes, it is possible to refinance an existing CalHFA loan. Refinancing an existing CalHFA loan is a practical option for homeowners in California seeking financial flexibility. The California Housing Finance Agency (CalHFA) provides various refinancing solutions, which may lead to benefits such as reduced interest rates, lower monthly mortgage payments, or adjusted loan terms to align with the homeowner’s current financial needs.

Key Considerations for Refinancing with CalHFA:

- Program Limitations: It’s important to note that as of July 1, 2019, CalHFA discontinued its resubordination program. This means all subordinate CalHFA loans must be paid in full if the first mortgage is refinanced, except under specific circumstances such as approval under a servicer’s loss mitigation program. Consult with a CalHFA-approved lender or financial advisor to understand how the discontinuation of the resubordination program might impact your specific refinancing plans and explore alternative solutions.

- Mortgage Credit Certificates (MCC): For eligible homeowners, CalHFA’s Dream For All Shared Appreciation Loan may offer the possibility of reissuing a Mortgage Credit Certificate (MCC). However, homeowners should carefully review the specific terms under which an MCC can be reissued. Review the specific terms under which an MCC can be reissued and consult with a professional to understand the implications and process for your situation.

- Refinancing Programs: CalHFA offers refinancing options like the CalHFA FHA and CalHFA Conventional Loans. These programs often feature deferred-payment junior loans, assisting with down payments and closing costs. Eligibility for these refinancing options requires adherence to certain criteria and state guidelines. Review the most current program details and eligibility criteria for CalHFA refinancing options on the CalHFA website or through consultation with a CalHFA-approved lender.

- Support for ADU Projects: Homeowners looking to build or renovate Accessory Dwelling Units (ADUs) may find CalHFA’s refinancing options particularly beneficial. The ADU Grant Program, aimed at boosting affordable housing, offers financial support for ADU construction or conversion. Refinancing a CalHFA loan could provide additional resources for such endeavors.

For California homeowners with a CalHFA loan who are contemplating refinancing, it is crucial to thoroughly explore and understand the available options and their respective eligibility criteria. While CalHFA presents a variety of programs tailored to diverse needs, careful consideration of the specific details and restrictions of each program is essential for making well-informed refinancing decisions.

What is the ADU bonus program in San Diego?

San Diego’s ADU (Accessory Dwelling Unit) Bonus Program is a strategic initiative aimed at bolstering the city’s affordable housing supply. This program incentivizes homeowners to construct ADUs on their properties, offering added benefits for those who agree to deed restrict their ADUs as affordable for very low-, low-, or moderate-income households for a 15-year duration.

Key Features of the ADU Bonus Program:

- Deed Restrictions: Homeowners who deed restrict their ADUs as affordable housing for specific income groups can build additional ADUs on their property. This strategy aligns with the city’s goal to make affordable housing more accessible.

- No Cap in Transit Priority Areas (TPA): In TPAs, for every affordable ADU built, homeowners are permitted to construct one bonus ADU, with no upper limit on the total number of ADUs.

- Outside TPAs: Homeowners can build one bonus ADU in exchange for one affordable ADU. However, no additional bonuses are provided beyond this in areas outside of TPAs.

- San Diego Housing Commission’s (SDHC) Involvement: SDHC runs an Accessory Dwelling Unit (ADU) Finance Program catering to low-income homeowners in the City of San Diego. This program provides financial aid in the form of construction loans and technical assistance, guiding homeowners through the ADU building process.

These incentives not only benefit homeowners but also contribute to the broader community by increasing the availability of affordable housing options in San Diego.

Further Resources and Information:

For more detailed information, the City of San Diego’s Planning Department and SDHC offer comprehensive resources. Homeowners can find guidelines on ADUs and JADUs, including the Companion Unit Handbook and Information Bulletin 400. Additionally, standard and permit-ready ADU building plans accepted by the City of San Diego are available, easing the construction process.

Consulting these resources early in your planning process can provide valuable insights into requirements and available support and streamline your journey to building an ADU.

Conclusion

San Diego’s ADU Bonus Program is a significant step towards creating more affordable housing options in the city. By incentivizing homeowners to build ADUs and providing necessary support and resources, San Diego is addressing housing affordability and promoting sustainable urban development efficiently.

How can I stay current on CalHFA’s programs, news, and updates?

For individuals interested in California’s ADU Grant and Loan Programs, staying updated with the latest information from the California Housing Finance Agency (CalHFA) is crucial. Here are some effective ways to keep abreast of CalHFA’s offerings and updates:

- eNews Announcements: A great way to receive current information is by subscribing to CalHFA’s eNews Announcements. This service ensures you get email notifications about recent announcements, program updates, and other essential news directly in your inbox. You can subscribe to CalHFA’s eNews Announcements on their website. Consider setting up email filters to ensure these updates don’t get missed in your spam folder.

- Social Media Channels: Following CalHFA’s social media accounts on platforms like X (formally known as Twitter) and Facebook is another convenient way to stay updated. These platforms often share timely updates, news, and changes related to the ADU Grant and Loan Programs, making them a valuable source for instant information. While social media is a great way to receive quick updates, always verify any important information through official CalHFA channels or contact them directly for confirmation.

- Regular Website Visits: The CalHFA website is a comprehensive resource for the latest on their programs, including press releases and project bulletins. Regularly visiting their website can provide you with detailed insights into various loan programs, resources for ADU projects, and other initiatives beneficial for those exploring housing options in California.

- Program Bulletins and Updates: CalHFA periodically releases Program Bulletins and updates that provide essential information about changes in policies, interest rates, and program guidelines. Keeping an eye out for these bulletins on their website or through their eNews service can be immensely helpful. Familiarize yourself with the section of the CalHFA website where Program Bulletins and updates are typically posted so you can easily access the latest information.

- Workshops and Webinars: CalHFA occasionally organizes educational workshops and webinars that can provide valuable information about their programs and housing opportunities. Participating in these events can offer deeper insights and direct interaction with housing experts. Check the CalHFA website regularly for announcements about upcoming workshops and webinars, and consider signing up for any available notifications or alerts about educational events.

In summary, by leveraging these various channels, you can stay well-informed about the evolving landscape of housing finance options in California. Whether you’re considering applying for an ADU grant or looking for financing options for your housing project, staying updated with CalHFA’s latest news and programs will help you make informed decisions for your housing needs.

Success Stories

Many homeowners in California have benefited from the ADU Grant Program, turning their properties into comfortable, inviting spaces for their families and guests. One such story involves a family in Poway who enlisted the help of ADU Contractors to design and build their dream accessory dwelling unit.

Another example is a homeowner in La Jolla who partnered with a La Jolla ADU Contractor to create a smaller home on their property. This not only added value to their land but also allowed them to make the most of available space. Their ADU journey was smooth, thanks to the expert guidance and craftsmanship provided by the builder.

In Encinitas, a fortunate homeowner collaborated with an Expert ADU Contractor to construct an additional unit to their home. This new space improved their overall living experience and increased the property’s appeal.

Carmel Valley is no stranger to success stories, as residents there have also taken advantage of the ADU Grant Program. One example showcases a homeowner who worked closely with ADU Contractors in Carmel Valley to bring their ADU vision to life. The resulting structure added both function and beauty to their property.

These success stories demonstrate the potential of the ADU Grant Program to transform properties across California. Leveraging experienced ADU Design and Builder Contractors can make the journey toward building an accessory dwelling unit a positive and rewarding experience for homeowners.

Conclusion: Navigating California’s ADU Programs for Enhanced Housing Solutions

In recent years, the State of California has significantly expanded its efforts to facilitate the construction of Accessory Dwelling Units (ADUs), making them more accessible and financially viable for homeowners. The evolving landscape of these initiatives, especially through the CalHFA ADU Grant Program, has been instrumental in addressing the state’s housing affordability and availability issues.

Key Highlights:

- Updated Grant Amounts: The CalHFA ADU Grant Program now offers up to $40,000 to qualifying homeowners, with a recent focus on assisting those earning up to 80% of the Area Median Income (AMI). This adjustment is crucial in making the program more accessible to low-income homeowners, aiding in covering crucial predevelopment expenses like permits, architectural designs, and soil tests.

- Loan Opportunities and Approved Participants: Beyond grants, California also provides diverse loan options, including those facilitated by a network of approved lenders and non-profits. These financial tools are pivotal in bolstering the state’s housing market by making ADUs more attainable. Consult with financial advisors or approved lenders to understand which loan options best fit your financial situation and project needs.

- Expert Guidance and Sustainable Development: Embarking on an ADU project requires thorough planning, expert input, and adherence to sustainable development practices. Professional home remodeling and design contractors in regions like San Diego play a vital role, guiding homeowners from design to completion and ensuring compliance with all regulations. Seek out professionals with specific experience in ADU projects to ensure you receive the most relevant and effective guidance for your unique project.

- Income Opportunities Through ADUs: ADUs offer homeowners a pathway to generate additional income through rental opportunities, contributing to a more sustainable and economically diverse housing market in California.

In Summary, California’s ADU programs, comprising grants and loans, are strategically crafted to ease housing shortages and foster responsible property development. Homeowners are encouraged to leverage these opportunities to enhance their property values and contribute to a more sustainable living environment across the state.

By staying informed and working with experienced professionals, homeowners can navigate these programs effectively and transform their property to meet their needs and those of the broader community. As California’s ADU programs continue to evolve, staying updated on program changes and new opportunities will be key to making the most of these initiatives.

Frequently Asked Questions

Does ADU increase property tax in California?

Yes, constructing an Accessory Dwelling Unit (ADU) on your property may lead to an increase in property taxes. This is because the construction of an ADU often results in an increase in the property’s value, and property taxes are typically based on the assessed value of the property. For a precise assessment, consider consulting your local assessor’s office or a property tax advisor.

How much does an ADU increase property taxes in California?

The exact amount by which an ADU may increase property taxes depends on the value added by the ADU and the local property tax rate. Each jurisdiction in California has its own tax rate, so the increase may vary based on your location. The increase in property taxes can be calculated by multiplying the increased assessed value by the local property tax rate. For a more accurate estimate tailored to your property, you might want to contact a local tax assessor or a real estate professional.

What is the maximum grant amount available through the California ADU Grant Program?

The California ADU Grant Program can provide up to $40,000 in assistance for predevelopment and non-reoccurring closing costs associated with the construction of an ADU. These costs may include items such as site preparation, architectural designs, permits, soil tests, impact fees, property surveys, and energy reports.

Where can I find the application forms for the CalHFA ADU Grant?

Information on the CalHFA ADU Grant application process and forms can be found on the CalHFA website. Homeowners interested in the program should visit the website for complete details and instructions on how to apply.

Are there any lenders participating in the CalHFA ADU Grant program?

Yes, there are lenders that participate in the CalHFA ADU Grant program. To find a participating lender, you can refer to the list of approved lenders provided on the CalHFA website.

Is the California ADU amnesty program still available?

As of the time of writing, it is unclear if the California ADU amnesty program is still available. The program aimed to help homeowners legalize unpermitted ADUs by providing assistance with the permitting process. It is recommended to check with your local jurisdiction or a housing expert for the most current information on this program.

Who qualifies as a first-time homebuyer?

A first-time homebuyer is generally defined as someone who has not owned a home in the previous three years. However, specific definitions and eligibility requirements may vary depending on the program or financial assistance. It is best to consult with the specific program or lender for their eligibility criteria.

If you’re considering building an Accessory Dwelling Unit (ADU) and navigating the complexities of grants and loans in California, don’t hesitate to contact us at Kaminskiy Design and Remodeling.

Our team of experts is ready to guide you through every step of the process, ensuring you make the most of the available programs. We’re committed to turning your vision into reality while maximizing your investment.

Give us a call at (858) 271-1005, or to schedule a consultation, simply fill out our contact form. We look forward to partnering with you on your ADU project!

Last updated on January 2, 2024

Kimberly Villa is the Operations Manager at Kaminskiy Design and Remodeling, where she has spent more than a decade involved in projects from pre-design through post-construction. Her experience in the remodeling industry spans nearly two decades across both East Coast and Southern California markets, giving her a firsthand view of how San Diego remodels unfold, from the first budget conversation to the final walkthrough. That day-to-day experience shapes the articles she writes for the Kaminskiy blog, where she helps homeowners make informed decisions before, during, and after a remodel. Before publication, each article is reviewed for accuracy by a Kaminskiy team member with relevant project expertise, such as a licensed architect, certified designer, or project manager.